- This topic has 4 replies, 3 voices, and was last updated May-223:03 pm by

Sophie Macon.

-

AuthorPosts

-

-

Up::4

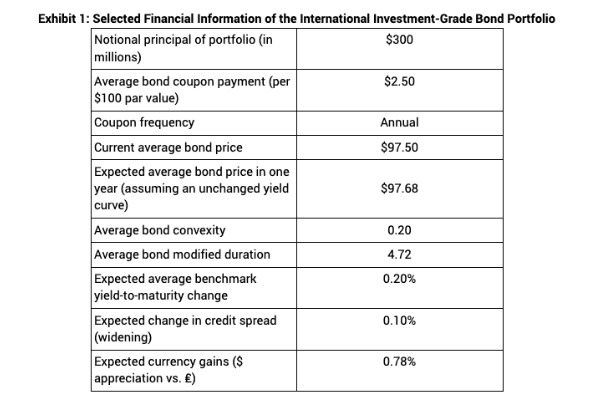

Could somebody help on how the result to this question is choice C? I al a bit lost in return computation. I cannot find 2.1%. Thanks

-

-

-

Up::0

I am guessing….

Coupon yield = 2.56%

%change in bond price = 0.18%

Credit spread change = -0.47%

YTM change = -0.99%

Forex = 0.78%

total = 2.06%

I definitely want to defer to another for a correct answer.

-

Up::0

Hey @jerrylow, @jewelswizz, thanks for spotting this error, it seems that we have missed out Q29’s explanation in depth in the email. You seem right @jerrylow

Here’s the explanation and workings, hope this helps!

Total expected return = Rolling yield ± E(Change in price based on investor’s benchmark yield view) ± E(Change in price due to investor’s view of credit spread) ± E(Change in price due to investor’s view of currency gains or losses)

Rolling yield = Coupon income + Rolldown return

Coupon income = Annual coupon payment/Current bond price

= $2.50/$97.50

= 2.564%

Rolldown return = (Bond pricet=1 – Bond price t=0) / Bond price t=0

= (97.68 – 97.50)/97.50

=0.185%

Therefore, Rolling yield

= 2.564% +0.185%

= 2.749%

E(Change in price based on Steven’s benchmark yield view)

= [–MD × ΔYield] + [1/2 × Convexity × (Yield)2]

= [-4.72×0.0020] + [1/2 × 0.20 × 0.00202]

= -0.94396%

E(Change in price due to Steven’s view of credit spread)

= (–MD × ∆Spread) + [½ × Convexity × (∆Spread)2]

= (-4.72×0.0010) + [1/2 × 0.20 × 0.00102] = -0.47199%

E(currency gains or losses) = 0.78% (given)

Therefore, total expected return

= 2.749% -0.944% -0.472% + 0.78%

= 2.11%

-

-

AuthorPosts

- You must be logged in to reply to this topic.